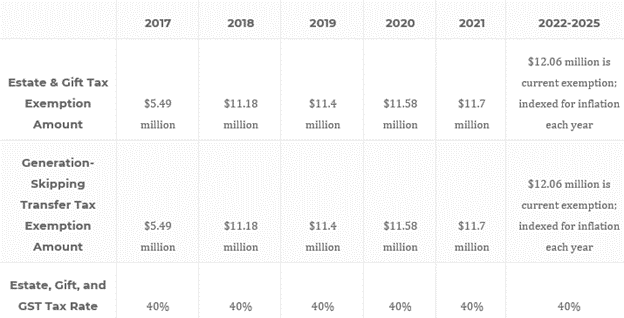

To stay on top of changes to federal estate tax laws, gifts, and generations skipping tax exemptions (GST), it may be necessary to revisit and update your estate plan annually. On the first day of 2026, the federal tax assessment on estates worth at least $11.7 million, indexed for inflation annually, will revert back to pre-2018 exemption levels. Any estate valuation over this amount will trigger a 40% federal estate, gift, and GST tax rate. As tax reform law affects your estate planning strategy, it is wise to review your unique estate situation routinely.

Changing Estate Tax Exemption Amount 2017 – 2025

Estate Planning Strategies to Deal with New Tax Laws

Even if your current taxable estate is under 12.6 million, you must still plan pivoting strategies for future estate tax changes. When the current federal tax laws sunset on January 1, 2026, the new laws will significantly change various estate planning techniques. Predicting exact numbers is impossible; however, some proposals plan to reduce estate and gift tax exemptions from $12.6 million per individual taxpayer to $3.5 – $6.85 million. Focusing on your plan today can help you position your estate for the changes ahead. Lifetime gifting is a strategy that still makes sense even if you are well below the $12.6 million threshold.

Estate Tax Strategies Designed for Your Situation

Additionally, checking your existing estate plan documents to ensure they will align with your goals is crucial as current federal exemptions can demonstrably affect your plan. For example, suppose your will states an amount equal to your remaining federal exemption will go to a “bypass trust” or “credit shelter” for your surviving family. In that case, the remainder passes outright to your spouse. Therefore, if you die with a $10 million estate today and used no exemption during your life, the whole of the $10 million would pass in trust under current law. Aside from not being aligned with your wishes, depending on your state of residence, this scenario may subject your estate to a higher state estate tax upon your death. Understanding the complexity of these tax laws and how they affect your estate plan is critical for protecting your family’s inheritance.

Gifting Amounts Over the 12.6 M Threshold

Suppose your taxable estate is currently over the $12.06 threshold. In that case, the most straightforward strategy is to begin giving away more money, remembering that current exemption amounts provide a limited opportunity to make these larger tax-free gifts. Gifting strategies remove the gifted asset from your taxable estate and all appreciation on the asset from the gift date until you die. Reviewing your current estate documents with your attorney can identify if these changes are warranted.

Many pre-2018 tax-saving strategies still make sense under the current law. Annual gifting exclusions of $16,000 per recipient, and $32,000 if spouses split their gifts, are permissible without using any lifetime exemptions. Annual exclusions for medical or educational purposes are also a viable strategy remembering that contributions to a 529 education plan will eat into the annual exclusion amount. Known as “Med/Ed” Gifts, variable amounts are gifted for limited purposes. The payment, however, must be made directly to the educational or medical provider. Your estate lawyer can help you understand these gifting “freebies” and how they can complement your estate planning strategy.

Estate Tax Planning with Trusts

Suppose you employ a Crummey Trust strategy for gifting while minimizing tax consequences. In that case, the annual exclusion gift to a trust instead of outright gifting requires a Crummey Trust notice to beneficiaries in connection with the gift. There are many trust types and how they may be useful to your estate depends largely on your family and financial situation. Tax minimizing estate trusts can also include:

- Spousal limited access trust (SLAT)

- Intentionally defective grantor trust (IDGT)

- Dynasty Trust

- Intrafamily loans

- Grantor retained annuity trust (GRAT)

Estate Planning and Tax Laws Vary by State

At a state level, your estate taxes will depend on which state you reside in and if you have properties in multiple states. Each state has different gift and estate tax laws. Your estate planning attorney can explain the discrepancies between federal and state law exemptions amending your estate documents accordingly. If you live in a state with estate taxes, it is crucial to address these laws and how they affect your federal estate tax planning strategies.

Because of the decision to sunset existing tax laws, even without Congressional action, the exclusion rate will reduce by half effective January 1, 2026. While federal exemptions are still relatively high, there is a short time frame to reduce your taxable estate through additional gifting or establishing new trusts. Your estate planning attorney can determine how to optimize your gifting strategy and if your estate planning documents require significant changes.

For assistance, please contact our Albuquerque office at (505) 830-0202